The Timber Log is a quick overview of Timber Point Capital’s weekly investment meeting. If you would like to join the call or have questions about the content, please reach out to Patrick Mullin at pmullin@timberpointcapital.com

The information contained herein does not constitute investment advice or a recommendation for you to purchase or sell any specific security.

Market volatility remains subdued, single stock volatility seems more elevated…

- Broader market performs well, S&P 500 up 1.47% MTD

- Russell 2K down 1.7% MTD – breadth is particularly poor among small cap stocks

- Small cap earnings have been very strong, supply constraints are an issue

- Will we see revenue estimates cut in lead up to 3Q earnings? We don’t think so.

- Management teams pivoting to a multiple source strategy, pivot from China continues

- Supply chain reorientation will take years to fully execute, not all coming back to US

Where will economic growth come from as Y/Y comparisons become difficult?

- Growth will be driven by large cap names with sustained, secular growth prospects

- Tech has been leadership over last decade…will continue to outperform

- S&P 500 and 30-year Treasury have remained correlated over past 4-5 months

- Yields seem to have put in a bottom now, TLT not rallying when market moves up

- VERY recent divergence in correlation is interesting….mkt up, yields up

Int’l Markets shrugging off geopolitical risks and potential leadership void in U.S

- Afghanistan – if continues to go sideways, budget deal could be in jeopardy

- U.S. citizens better remain unharmed and able to exit – if not, big market concern? Yes.

- Investing in China – will need 5-year plan and identify sectors best positioned to benefit

- At some point there’s got to be value in China…right? We believe so.

- Very hard to get insight and/or clarity on policy out of China = compressed multiples

- Will other nations be emboldened to “push back” on US? Certainly, China will, as have seen with recent outreach to Taliban government

Repo market activity suggests Fed draining liquidity before start of tapering…

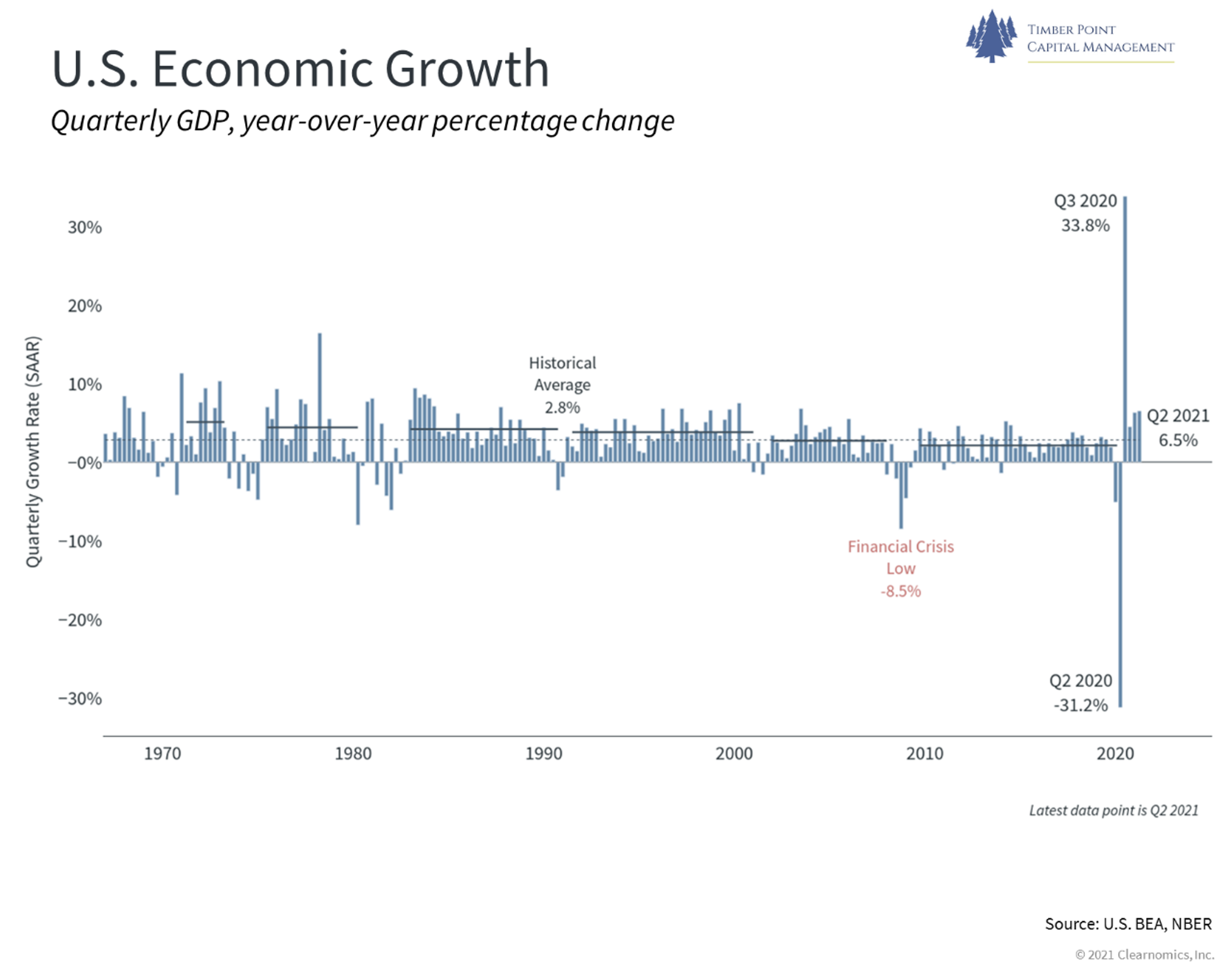

- Econ growth will slow, return to normalized growth healthy for markets in long run

- Downwardly revised GDP growth projections…estimate of 3.3% for ’22 & 2.25% for ’23

- Normalized growth will separate truly outstanding businesses from liquidity driven

- Is above thought why breadth is so poor in small cap market? Could be…

- When will FED begin tapering its bond purchases? Will delay as long as possible

- Current excess liquidity in capital markets putting cap on yields…will resolve slowly

- Keep eye on savings rate, now elevated – retail data says consumers are pulling back

New Covid delta variant Is spreading rapidly…cases are ramping up fast in US

- Delta variant a challenge for economic growth and “vaccine recovery” play names

- Fear of potential lockdowns could be catalyst for dislocation in markets

- May cause Fed to hold on to low-rate policy for longer

- Dollar has been strong as leading vaccine rollout…could change as ROW catches up

- Israel delta suggests vaccines less effective in transmission but limit serious symptoms

- UK opened economy in mid-July – cases are up but hospitalizations and deaths subdued

Recent Comments