The Timber Log is a quick overview of Timber Point Capital’s weekly investment meeting. If you would like to join the call or have questions about the content, please reach out to Patrick Mullin at pmullin@timberpointcapital.com

The information contained herein does not constitute investment advice or a recommendation for you to purchase or sell any specific security.

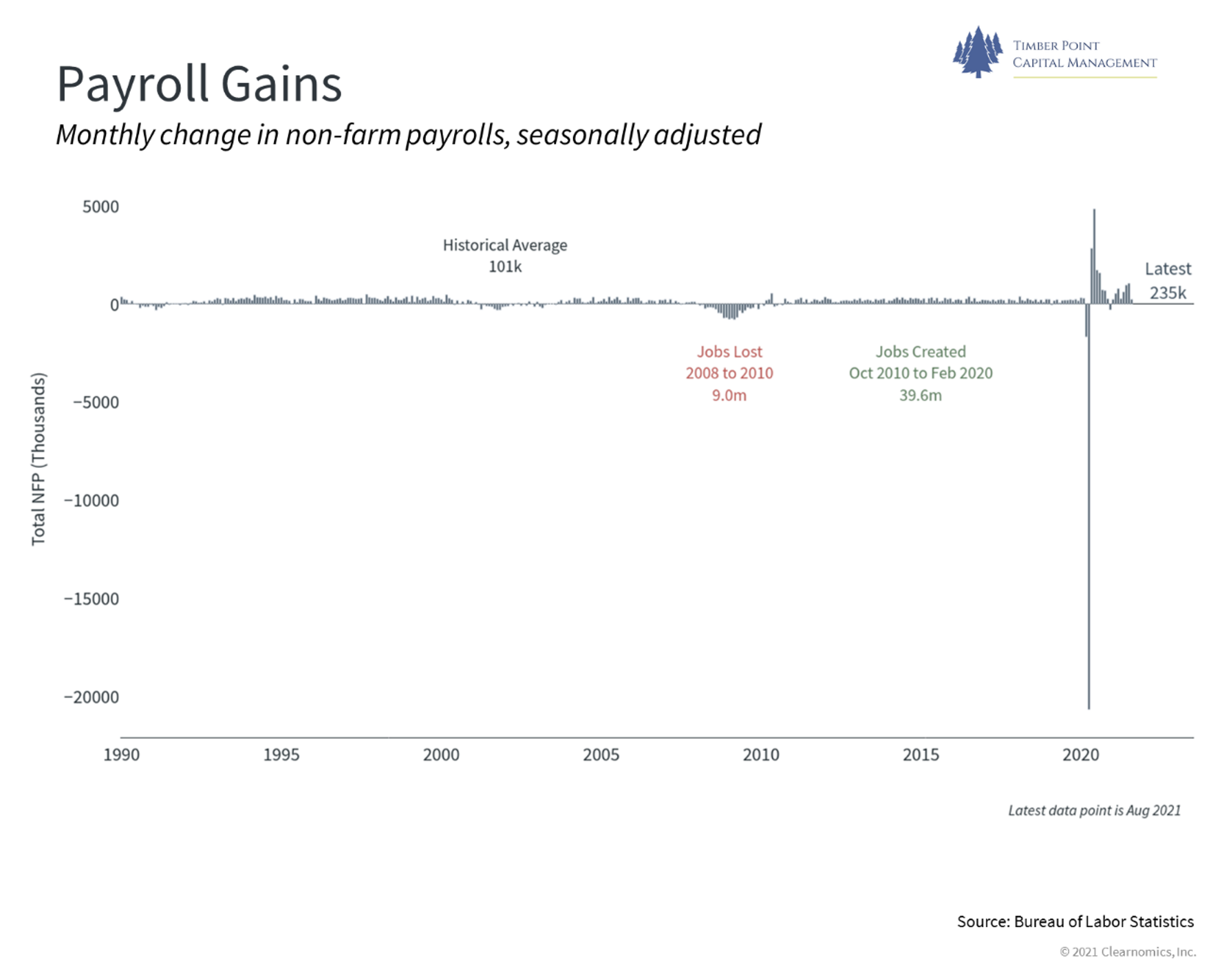

Payroll numbers disappoint in August…just another supply clog?

- Unemployment benefits winding down, employment like to pick up again

- But economy is slowing – treasury rally, growth stocks and technology outperform

- Economy weighed down by regulation, government intervention, higher tax talk

- Even censorship of speech has chilling impact on business activity/risk taking

- Minimum corporate tax rate of 15%, will make US one of highest corp. tax payors

- Return to Obama tax structure means 3% growth rates could slow to 1% – 2%

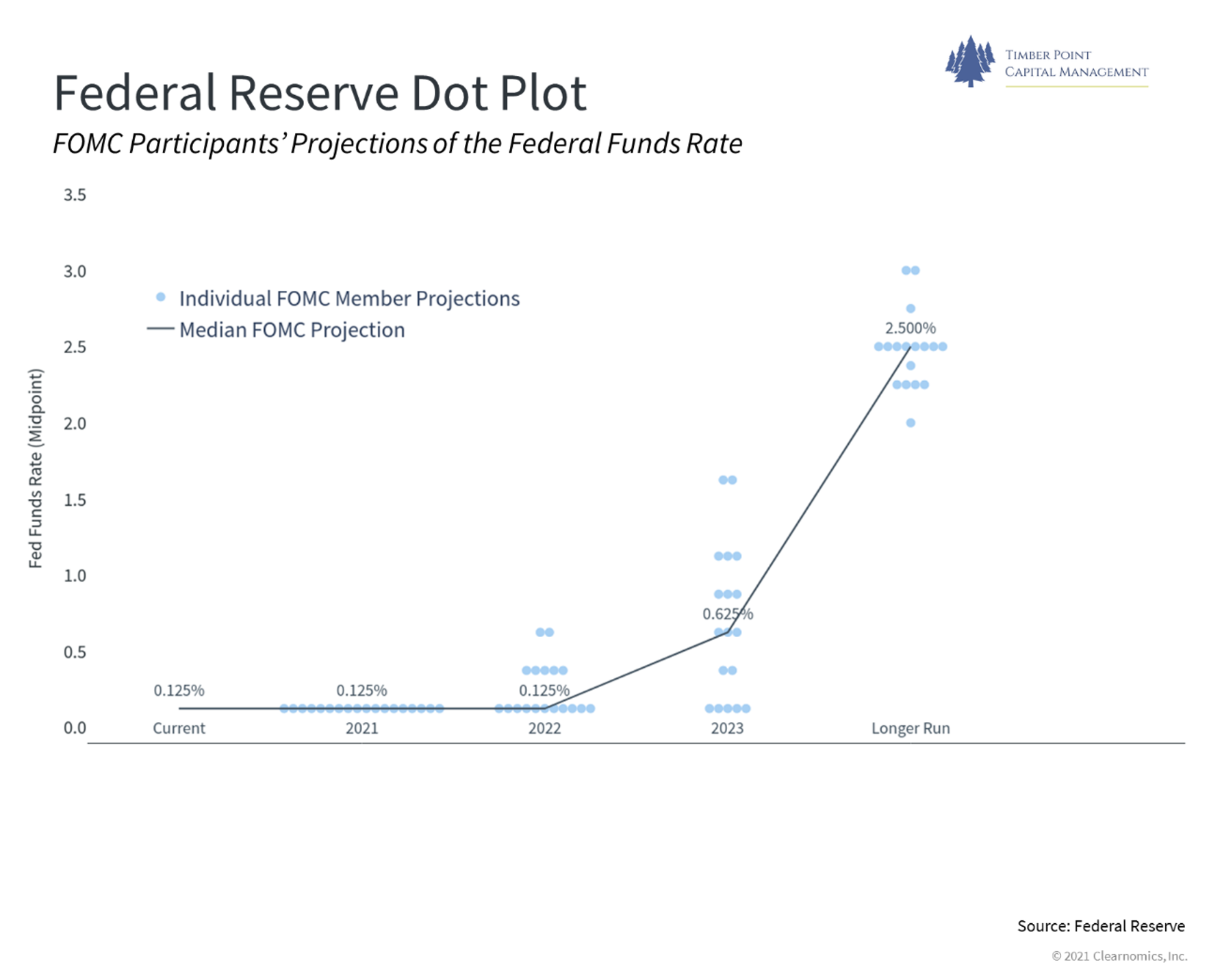

Monetary Policy – Yes to taper in 2021, no to rates blowing out

- Powell wants to be re-nominated – we believe he will be

- Fed will “listen” to admin desires for continued liquidity as move into mid-term elections

- Taper may begin later 2021, but will be a slow, protracted removal of liquidity

- According to Powell, Dot Plot to be “taken with a big grain of salt”

- “Substantial further progress” on unemployment and inflation needed for hikes

- Next Fed meeting September 21/22 – recent unemployment report slows “progress” toward tapering

- Recovering supply chain will cool inflation fears and economy

- We see continued “lower for longer” interest rate environment, valuations will remain higher than long term averages

- Need continued earnings follow through to sustain elevated valuations

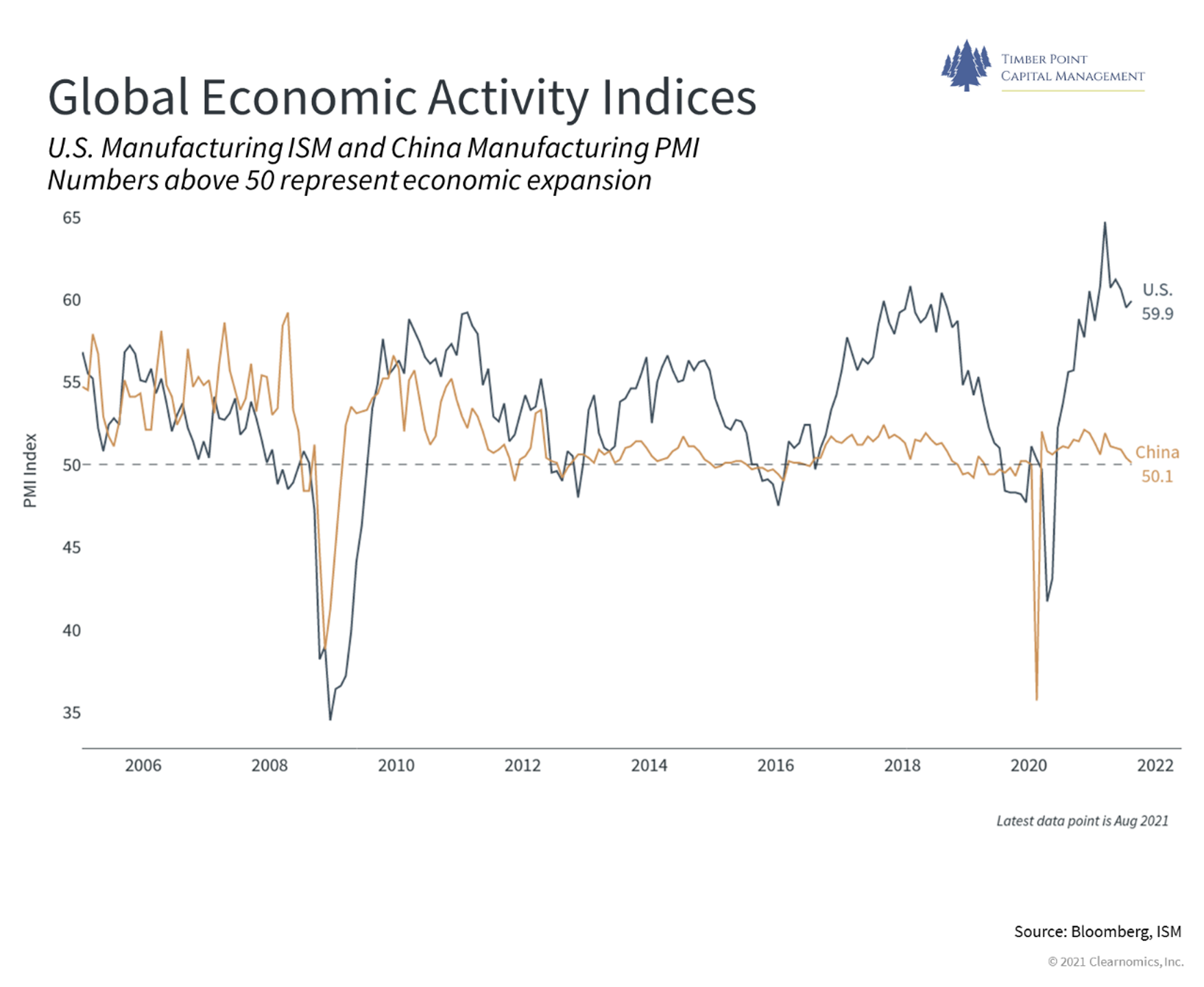

EM and China stocks are rallying – remain positive on China equities

- Overcorrection occurred; opportunity given large valuation discrepancy

- Understand valuations will be impacted but mass exodus leaves stocks overdone

- China providing example of regulatory measures that others are watching closely

- Will global ex-China stocks be subject to China actions? Absolutely…

- China going after Canada Goose, when target NKE, CAT, SBUX?

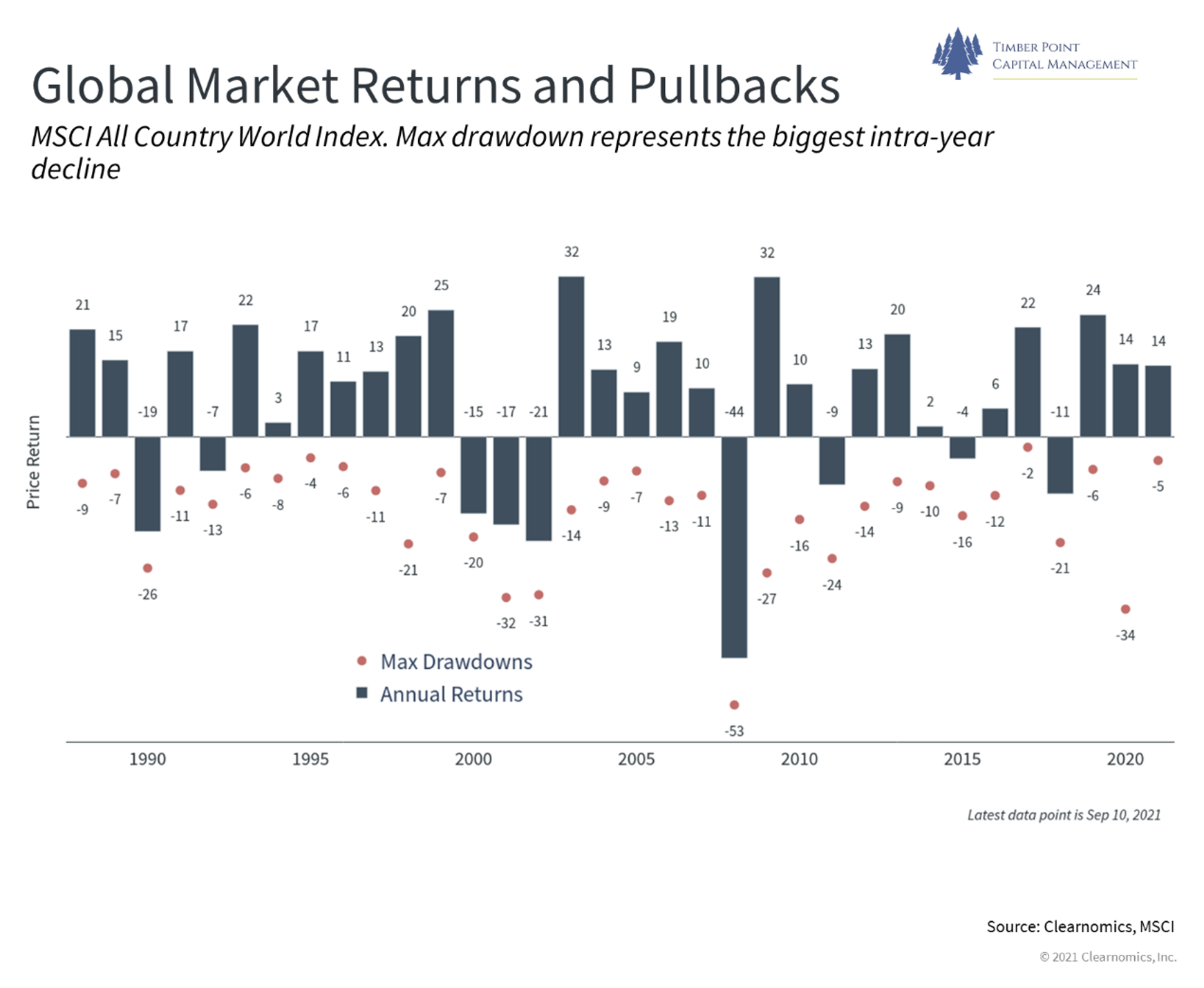

Country returns QTD are a mixed bag – hard to identify key drivers

- Turkey and India are best two; China and Brazil are two worst

- Netherland and Ireland best two in Europe, Germany and Italy the worst

- Max intra-year drawdown for MSCI- ACWI is at lows going back 30 years

- Vaccine related issues still play a part in capital movement

- Hopes for economic recovery in global markets – still waiting for Japan growth recovery!

- TPCM portfolios still skewed to risk assets, US equities and small/mid cap space

Recent Comments